What is a corporation?

If you’re new to the world of business, and eCommerce, then there are plenty of terms, ideas, names and acronyms to get your head around. With that in mind, and knowing that many of our Avasam sellers do other work alongside their DropShipping business, we thought we would set up a few shorter posts that explain some of the key terms and ideas.

While some of these posts will absolutely help you with getting started, when it comes to anything legal or tax-related for your company, we always advise that seek out specialist advice from an accountant or appropriate professional. Doing so will help ensure that your tax liabilities are registered correctly with HMRC, or with whichever entity is responsible for collecting taxes in the country you are in, and that you pay the correct amount of tax.

For this post, we’ll be focusing on corporations and different types of business within the UK, since that’s where the Avasam team are based. However, in different countries there are different rules and regulations – so always do your due diligence and take advice where appropriate.

What is a corporation?

A corporation is a group of people who are authorised to act on behalf of the company. They have rights and liabilities that are distinctly separate from the individuals that make up the corporation.

Features of corporations

There are several common characteristics that can help to define a business corporation. These include:

- Transferrable shares

- A central management team under a board structure

- Limited liability – meaning the shareholders and employees are not liable for debts owed to the corporation’s creditors if the business fails

- Legal personality – which means the corporation is recognised as having rights and responsibilities in the same way people do. Should criminal offenses occur due to a corporation’s action or inaction, they can be found guilty of such acts as fraud and manslaughter.

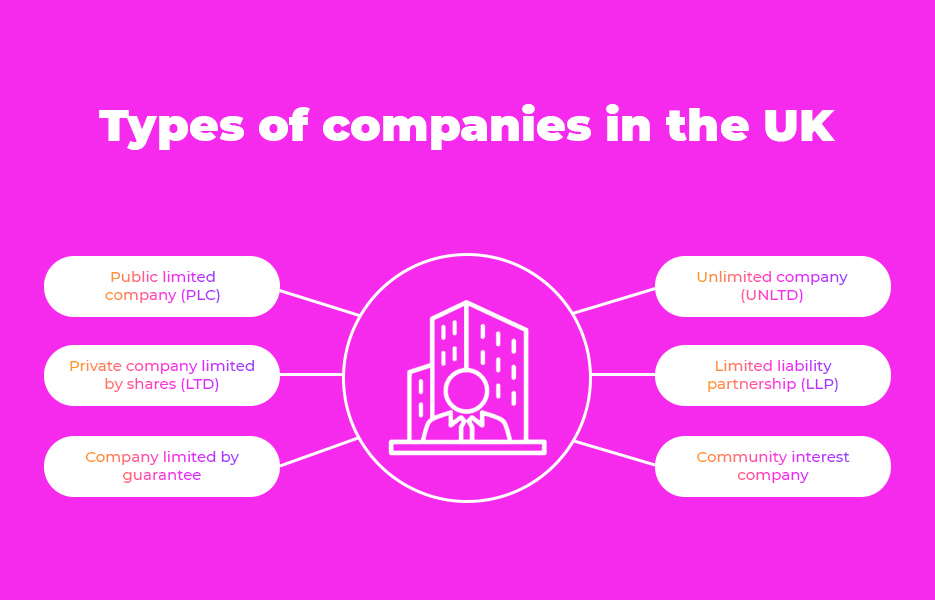

Types of companies in the UK

There are several types of companies in the UK, and it is important to know the difference and that you register your business correctly. The different types of company have different legal requirements, ownership requirements and necessities for what should happen if the company goes into liquidation (closing the business and distributing assets amongst the claimants), as well as having different tax liabilities.

Public Limited Company (PLC)

This is a type of corporation that makes shares available to the public to be able to buy. The sale of theses shares is not restricted – anyone can buy them. Essentially, anyone who has invested in the company is only financially liable for the amount that they have invested. Before a PLC is able to start business, it needs to have allotted shared to the value of at least £50,000.

Private company limited by shares (LTD)

Private companies cannot be owned by any members of the public outside the company. The company will be owned by an NGO (a non-government organisation) or a reasonably small number of shareholders, with the sale of any shares being handled privately. Financial liabilities are restricted to the amount that the investor has added to the company.

Company limited by guarantee

This is a very different type of company. These companies are usually reserved for smaller, non-profit organisations, and those that don’t have shareholders. Any individuals who invest in a company limited by guarantee act as guarantors, and will agree to contribute a given amount towards the winding up of a company, if such an event occurs. Legally, in the UK these companies must include ‘Limited’ in their names – although there are occasions when exceptions can be made, such as when companies are not sharing their profits with their members.

Unlimited company (UNLTD)

With unlimited companies, there are no formal restrictions on the amount of money that shareholders should pay if a company goes into liquidation. If the company is formally liquidated, any shareholders are responsible for paying for the company’s outstanding financial liabilities, no matter how much they have invested in the company.

Limited Liability Partnership (LLP)

LLPs are treated as incorporated bodies where some, or all of the partners have limited liabilities. That means they are only responsible for their own actions, misconduct or negligence. A more traditional partnership model would hold all the partners responsible collectively. In addition, the partners can directly manage the business, unlike other types of companies where shareholders have to elect a board of directors, and the board employs people to manage the company for them.

Community Interest Company

This type of company is set up to use their assets, and their profits with the intention of doing good for their community. They’re pretty easy to set up, and any profits are generally put back into the company so that they can improve the services, and resources that they offer the community.

Why turn your business into a corporation?

“Should I set up as a limited company?” is a question that accountants hear pretty regularly. And for good reason, since there are lots of advantages to switching to a corporation. But it isn’t always a straightforward decision, so let’s take a look at some of the things you’ll need to think about, and discuss with your accountant before you get started. We’ve listed these first considerations as advantages – because generally they are – but you might find for your business as challenges too. (don’t forget that challenges can be positive!)

Legitimately paying less tax

This is the biggest advantage for most people. As the director and shareholder of a limited company, taking a smaller salary and drawing your income from the business in the form of dividends means you can minimise the amount of National Insurance Contributions (NICs) you need to pay. Limited company dividends are not subject to NICs.

In addition to this, corporations can pay for employee executive pensions as a legitimate business expense, so they are made before tax is deducted.

Distinct entity with limited liability

Your corporation will be completely separate from you. That means your company bank account, assets and transactions are purely for business and are separate from the interests of any shareholders.

Because of that, as long as there has been no fraud, if the business is wound up, you will not be personally liable for any debts belonging to the business. You are protected personally and you won’t be expected to pay for any of those outstanding debts.

Trading name

As the business is registered with Companies House, the name is protected by law. Other businesses will be blocked from using the same name, or anything that is too similar.

Professionalism

Depending on the industry you’re in, some companies may view corporations as more professional than sole traders or partnerships, and choose to only deal with limited companies.

Challenges of turning your business into a corporation

Not all of theses issues will be a challenge for every business. For example, if you’ve already got someone with tax or accounting experience working for you who can do the set up and handle your accountancy needs, then the only cost you might have to meet is that person’s wage. Your accountant might identify other challenges for your business too though – every business is different!

Complexity

Although for professionals who set up companies regularly, setting up a business as a limited company can be challenging for people who haven’t done it before. In addition, limited company accounts are much more challenging than for other businesses. Mistakes can be costly – and penalties from HMRC can be severe if deadlines are missed. Using an accountant or tax professionals is essential.

Costs

Since we have mentioned using accountants or tax professionals, that’s a major cost. But considering your accountant can file your company tax returns, ensure your corporation tax is paid, and file your VAT returns for you – which is a considerable amount of work, and can be expensive if done incorrectly – it is a cost worth paying.

Ownership

The old phrase about too many cooks spoiling the broth can apply to limited companies. The more shareholders, the more opinions to be taken into account – which can cause difficulties when challenging, or pivotal decisions or actions need to be taken.

Public records

Information about the owners of a company have to be registered with Companies House, and those details are accessible by anyone. Where privacy is a concern, this could be problematic.

How to form a corporation

It’s a relatively fast process to incorporate your business – usually the process takes less than 24 hours. You simply need to apply to Companies House. There may be additional information required, so if you want to ensure you have incorporated by a certain date (for tax planning) then it’s a good idea to leave a few days to a week to complete the process.

Depending on the business, you might decide to use an accountant or other professional to help with getting the corporation set up. They are able to help ensure your documentation is completed correctly before it goes to Companies House, which is likely to minimise the amount of time it takes for the process to be completed.

Who needs to be involved in helping you create your corporation?

You will want to work closely with your accountant (although a successful business usually does!) to ensure that deadlines are not missed. There are other deadlines that you’ll need to keep in mind, such as the personal tax year (April 6th to April 5th the following year). Like many other companies, you may decide to line up your financial year-end close to the tax year-end, so that all the accounting, payroll and tax work can be done together. However, not all businesses are the same, and so consulting with a professional is a good idea to ensure your setup is right.

In terms of other individuals to be involved, it will differ from company to company – so begin discussions with your accountant and work according to what they advise.

What happens after you’ve created your corporation?

Well obviously, running business as usual is a good start – you already know what you need do day to day, and you’ll want to keep building that success! But you’ll have extra work to do when it comes to your taxes.

If you’re in the UK, corporations pay a separate type of tax on their profits – corporation tax. It’s paid on all profits, from trading profits – the everyday profits that the business creates, to any profit made on investments, or money made from selling assets.

Corporation tax has to be paid by a certain date – which is usually nine months and one day after your accounting period ends. The tax return must be completed within 12 months of the end of the accounting period.

You can find out more about corporation tax in the UK here, but unless you’re a trained accountant yourself, you’re almost certain to benefit from engaging with a registered tax professional.

There’s a lot to learn about different types of corporations, but if you hadn’t already got the message – the biggest advice we can give you about setting your business up as a corporation is to consult with a tax professional or accountant before you make any decisions or take any action. There is a lot to lose if you get it wrong, so do it once and do it right.

DropShip products from verified suppliers to diversify your inventory and scale your eCommerce business